Motorcycle Insurance in San Francisco: A Complete Guide for Riders

Imagine you’re cruising down the vibrant streets of San Francisco on a sunny afternoon, the iconic Golden Gate Bridge in the distance. The city’s winding roads, stunning views, and diverse neighborhoods make it a thrilling place to ride a motorcycle. But as any seasoned rider in the Bay Area will tell you, the excitement of the open road also comes with its share of risks—think congested traffic, unpredictable weather, and high rates of vehicle theft.

That’s why having the right motorcycle insurance isn’t just a smart move—it’s an absolute must. In fact, California law mandates that every motorcyclist carry a minimum amount of liability insurance. Yet, with nearly 300,000 motorcycle accidents reported in the U.S. each year, and San Francisco being one of the highest-density cities in the state, sticking to just the basic coverage might not be enough to truly protect you.

In this guide, we’ll break down everything you need to know about motorcycle insurance in San Francisco—from understanding the legal requirements to choosing the best coverage options for your specific needs. Whether you’re a daily commuter or a weekend warrior, having the right policy can save you from costly repairs, medical bills, or worse, legal issues. Let’s dive into how you can ride safely, confidently, and with total peace of mind on the streets of this bustling city.

Table of Contents

Understanding Motorcycle Insurance Requirements in California

If you’re planning to ride a motorcycle in California, there are certain insurance rules you absolutely need to know. The state requires every rider to have a minimum level of liability insurance, but these basic limits are often just the tip of the iceberg—especially if you’re navigating the bustling streets of San Francisco.

California’s Minimum Motorcycle Insurance Requirements

As of November 2024, California mandates that all motorcyclists carry at least the following liability insurance:

Bodily Injury Liability:

- $15,000 per person

- $30,000 per accident

Property Damage Liability:

- $5,000 per accident

These requirements are in place to cover damages or injuries you may cause to others in an accident. However, it’s important to note that these minimums are set to increase. Effective January 1, 2025, the new minimum liability insurance requirements will be:

Bodily Injury Liability:

- $30,000 per person

- $60,000 per accident

Property Damage Liability:

- $15,000 per accident

This change reflects the state’s effort to ensure that insurance coverage keeps pace with rising medical and repair costs.

Penalties for Riding Without Insurance in California

Operating a motorcycle without the required insurance in California can lead to significant penalties:

Fines:

- First Offense: $100 to $200, plus penalty assessments.

- Subsequent Offenses: $200 to $500, plus penalty assessments.

Vehicle Impoundment:

Law enforcement has the authority to impound your motorcycle if you’re caught riding without insurance. Retrieving your vehicle would involve paying towing and storage fees.

License Suspension:

If you’re involved in an accident without insurance, the state can suspend your driver’s license until you provide proof of insurance and meet other reinstatement requirements.

SR-22 Requirement:

You may be required to file an SR-22 form, which is a certificate of financial responsibility, with the Department of Motor Vehicles (DMV). This often leads to higher insurance premiums.

These penalties underscore the importance of maintaining at least the minimum required insurance coverage to avoid legal and financial repercussions.

Why Minimum Coverage May Not Be Sufficient in San Francisco

While meeting the state’s minimum insurance requirements is mandatory, these limits may not provide adequate protection, especially in high-cost areas like San Francisco. Consider the following:

High Medical Costs:

Medical expenses in San Francisco can be substantial. In the event of an accident causing serious injuries, the minimum bodily injury liability coverage may not cover all medical bills, potentially leaving you financially responsible for the remainder.

Expensive Property Damage:

The cost of vehicle repairs and property damage in San Francisco is often higher than in other regions. The minimum property damage liability may fall short if you cause significant damage in an accident.

Legal Expenses:

If damages exceed your insurance coverage, you could be sued for the remaining amount, leading to costly legal fees and potential judgments against you.

Given these factors, opting for higher coverage limits and added options like uninsured motorist and comprehensive coverage is a smart move. Staying informed about insurance requirements helps you make the best choices to protect yourself on the road.

Understanding Types of Motorcycle Insurance Coverage in San Francisco

Whether you’re zipping through the Embarcadero or cruising down the iconic Lombard Street, riding a motorcycle in San Francisco brings a unique thrill. However, it also comes with risks, especially in a busy urban environment. That’s where having the right insurance coverage can be a lifesaver—both literally and financially. Let’s break down the key types of motorcycle insurance available and explain why each one is especially important for city riders.

1. Liability Insurance (Required)

This is the bare minimum coverage required by California law. Liability insurance covers the costs if you’re found responsible for causing injuries or property damage to others.

- Bodily Injury Liability: Covers medical expenses, lost wages, and legal fees if you injure someone in an accident.

- Property Damage Liability: Covers repairs if you damage someone else’s vehicle or property.

Why It’s Important in San Francisco: With high pedestrian traffic and dense roads, accidents can happen in the blink of an eye. Liability insurance ensures you don’t end up paying out of pocket for someone else’s hospital bills or vehicle repairs, which can be exorbitant in this city.

2. Collision Coverage

Collision coverage pays for the repair or replacement of your motorcycle if it’s damaged in an accident, regardless of who’s at fault.

Benefits:

- Covers damages resulting from collisions with vehicles, road hazards, or even fixed objects like guardrails.

- Particularly useful if you own a newer or expensive bike that would be costly to repair or replace.

Why It’s Useful in San Francisco: With narrow streets, steep hills, and plenty of distracted drivers, accidents can easily happen. Collision coverage protects your bike from fender benders, which are common in crowded neighborhoods like SoMa or North Beach.

3. Comprehensive Coverage

Comprehensive insurance covers damage to your motorcycle from non-collision-related incidents, such as theft, vandalism, natural disasters, or falling objects.

Benefits:

- Protects against damage from events beyond your control, like a tree branch falling during a storm or your bike being stolen.

- Covers damages from vandalism, which is more common in urban areas.

Why It’s Essential in San Francisco: The city has one of the highest motorcycle theft rates in California, especially in areas like the Mission District. Comprehensive coverage provides peace of mind knowing that if your bike is stolen or damaged while parked, you’re covered.

4. Uninsured/Underinsured Motorist Coverage

This coverage protects you if you’re in an accident caused by a driver who doesn’t have insurance or doesn’t have enough insurance to cover the damages.

Benefits:

- Covers your medical expenses, bike repairs, and other related costs if hit by an uninsured driver.

- Ensures you’re not left financially stranded if the at-fault driver’s insurance falls short.

Why It’s Valuable in San Francisco: With the high cost of living, many people in the city may be driving around with minimal insurance coverage, or worse, none at all. If you’re hit by an uninsured motorist while riding through busy intersections like Market Street, this coverage can be a financial lifesaver.

5. Medical Payments Coverage

This type of insurance helps cover your medical expenses if you’re injured in an accident, regardless of who was at fault.

Benefits:

- Covers costs for hospital stays, surgeries, X-rays, and even rehabilitation.

- Provides coverage for your passengers as well.

Why It’s Crucial in San Francisco: With congested roads and distracted drivers, the risk of injury is higher in urban settings. Medical bills can add up quickly, especially in a city known for its expensive healthcare. Having this coverage ensures that you won’t be buried under a mountain of medical debt.

Getting the right motorcycle insurance in San Francisco goes beyond legal requirements—it’s about protecting yourself and your finances. With the city’s high costs and unique risks, comprehensive and uninsured motorist coverage are smart investments for peace of mind.

Factors Affecting Motorcycle Insurance Rates in San Francisco

San Francisco is known for its steep hills, heavy traffic, and diverse neighborhoods, all of which can influence your motorcycle insurance rates. Insurers take into account a range of factors when determining premiums, so let’s dive into the specifics that can either lighten or inflate your costs.

1. Location Matters: Higher Rates in Densely Populated Areas

Your ZIP code plays a significant role in determining your insurance rates. Insurers look at factors like population density, crime rates, and accident statistics. For instance:

- SoMa (South of Market) and the Mission District are known for their high traffic volumes and elevated theft rates. Riders living in these neighborhoods may face steeper premiums due to the increased risk of accidents and motorcycle theft.

- On the other hand, if you live in a quieter neighborhood like Sea Cliff or Noe Valley, where crime rates are lower, you might benefit from reduced premiums.

Pro Tip: If you can park your motorcycle in a secure garage, it may help reduce your rates, especially if you live in high-theft areas.

2. Type of Motorcycle: The Bike You Ride Affects Your Rate

Not all motorcycles are created equal in the eyes of insurers. The type, model, and performance level of your bike can significantly impact your premiums.

- High-performance sports bikes and custom-built motorcycles often come with higher insurance rates because they’re more likely to be involved in accidents and are costlier to repair.

- Cruisers and touring bikes, which are generally used for leisurely rides, typically have lower premiums.

- Electric motorcycles may qualify for discounts due to their lower top speeds and eco-friendly attributes, but be prepared for potentially higher repair costs due to specialized parts.

If you’re considering a new bike, it’s worth checking the insurance costs beforehand—sometimes, the thrill of a high-performance model comes with a hefty price tag on your policy.

3. Rider Profile: Age, Experience, and Driving History

Insurers assess the person behind the handlebars, not just the motorcycle itself. Factors that impact your rates include:

- Age: Younger riders (especially those under 25) are statistically more likely to be involved in accidents, leading to higher premiums.

- Experience: Riders with more years of experience and a clean record are often rewarded with discounts. Conversely, if you’re new to riding or have a history of traffic violations, expect to pay more.

- Driving Record: A spotless driving history is like a golden ticket—it can earn you substantial savings on your insurance. On the flip side, past accidents or tickets can push your rates up.

Completing a motorcycle safety course not only makes you a safer rider but can also qualify you for discounts from many insurers.

4. How You Use Your Motorcycle: Daily Commuter vs. Weekend Rider

Your motorcycle’s primary use—whether it’s your daily ride to work or just a weekend toy—affects your insurance rate.

- Daily commuters face higher premiums since they spend more time on the road, increasing their chances of being involved in an accident.

- Occasional riders, who only take their bike out on weekends or for special trips, can benefit from lower rates because they pose less risk.

If you’re someone who clocks in minimal miles annually, ask your insurer about a low mileage discount. It could save you money.

5. Safety Features: Anti-Theft Devices and ABS

Equipping your motorcycle with safety features can be a game-changer for your insurance premiums.

- Anti-theft devices, such as GPS trackers, alarms, or disc locks, can lower your rates, especially in theft-prone areas of San Francisco.

- Anti-lock Braking Systems (ABS): Motorcycles with ABS are statistically less likely to be involved in severe accidents. Some insurers offer discounts for bikes equipped with ABS because they reduce the risk of skidding and losing control.

When buying a new motorcycle, look for models with built-in safety features. These features can reduce your insurance costs and provide added peace of mind on the road.

How to Get Cheaper Motorcycle Insurance in San Francisco

Owning a motorcycle in San Francisco is a thrill, but insurance can be pricey. Fortunately, there are several strategies to cut costs without sacrificing coverage. Here’s how to lower your premiums while staying protected:

- Bundle Your Policies

If you already have auto or home insurance, bundling with your motorcycle policy can save you money. Insurers reward loyalty with multi-policy discounts.

Pro Tip: Compare the bundled rate with standalone policies to ensure it’s truly cost-effective.

- Complete a Motorcycle Safety Course

Taking a certified safety course, like those offered by the California Motorcycle Safety Program (CMSP), can earn you discounts of 10-15%.

Local Options: Check out courses at San Francisco Motorcycle School or Bay Area Motorcycle Training for discounts and skill-building.

- Tap into Discounts

Look for hidden savings:

- Good Driver Discount: Clean record for 3-5 years? Lower rates await.

- Multi-Bike Discount: Insure multiple bikes under one policy.

- Military Discount: USAA and others reward veterans and active personnel.

- Low Mileage Discount: Weekend riders can benefit from lower premiums.

- Actionable Step: Ask your insurer about these—often, they won’t mention them unless prompted.

- Secure Storage for Your Bike

In theft-prone areas like SoMa and the Mission District, storing your motorcycle in a secure garage can reduce your premiums.

Extra Tip: Adding anti-theft devices like alarms or GPS trackers can further lower costs.

- Shop Around for the Best Rates

Insurance rates vary widely, so don’t settle for the first quote. Use tools like The Zebra or Compare.com, or consult a local broker for the best deals.

Money-Saving Insight: Get quotes before your policy renews and consider paying annually to save even more.

By using these strategies, you can enjoy the open roads of San Francisco without overpaying on insurance.

Common Mistakes to Avoid When Buying Motorcycle Insurance

Buying motorcycle insurance can seem simple, but rushing can lead to costly mistakes, especially in a city like San Francisco where theft and accidents are common. Here are the top mistakes riders make and how to avoid them:

- Underinsuring with Minimum Liability

Sticking to the minimum coverage might save you a few dollars upfront, but it’s like a helmet with a crack—it won’t protect you when needed.

Fix: Consider higher limits to avoid being stuck with medical bills and repair costs if an accident exceeds your coverage.

- Skipping Comprehensive Coverage in a High-Theft City

San Francisco has high motorcycle theft rates. Without comprehensive coverage, you’re on the hook if your bike is stolen or vandalized.

Fix: Add comprehensive coverage, especially if you park on the street or have a high-end bike.

- Not Disclosing Modifications

If you’ve customized your bike, those upgrades may not be covered unless disclosed.

Fix: Inform your insurer of modifications and consider accessory coverage. Keep receipts and photos to support claims.

- Ignoring Uninsured Motorist Coverage

Many drivers in San Francisco lack adequate insurance. If you’re hit by one, uninsured motorist coverage can save you from out-of-pocket expenses.

Fix: Adding this coverage is inexpensive and essential for protecting yourself.

- Overlooking Discounts and Failing to Review Policies

Skipping annual reviews can mean missing out on discounts for safe driving, policy bundling, or safety courses.

Fix: Review your policy yearly, ask about discounts, and shop around before renewing to ensure the best rates.

Resources for San Francisco Motorcyclists: Clubs, Safety Courses, and Scenic Routes

San Francisco is not just a city; it’s a playground for motorcycle enthusiasts. Joining local communities, practicing safety, and finding the best routes can all make your riding experience better, no matter how long you have been riding or how new you are to it. Here’s a curated list of resources to help you ride smart, stay safe, and make the most of the open road.

Motorcycle Clubs and Community Forums:

- San Francisco Motorcycle Club (SFMC): Founded in 1904, hosting rides and events for riders to connect and share experiences.

- Bay Area Riders Forum (BARF): An online hub for discussions on bike maintenance and local rides, ideal for new and seasoned riders.

- Dykes on Bikes® San Francisco: An iconic LGBTQ+ club since 1976, known for leading the city’s Pride Parade and fostering an inclusive community.

Motorcycle Safety Courses:

California Motorcycle Safety Program (CMSP): Offers beginner to advanced courses at multiple Bay Area locations, including City College of San Francisco.

Bay Area Motorcycle Training: Covers basic to advanced techniques with certified courses that can lower insurance premiums.

Pacific Motorcycle Training: Based in South San Francisco, focusing on street safety, defensive riding, and navigating city traffic.

Best Riding Routes and Scenic Spots:

- Highway 1 to Stinson Beach: A favorite for its coastal views and winding curves.

- Mount Tamalpais Loop: Perfect for riders who love twisty roads and sweeping vistas.

- Skyline Boulevard (Highway 35): Smooth roads with occasional ocean views along the Santa Cruz Mountains.

- Alice’s Restaurant Ride: A classic stop in Woodside, with scenic routes like Highway 84 and La Honda Road through redwoods.

Always check the latest information and road conditions before planning your ride, as circumstances can change.

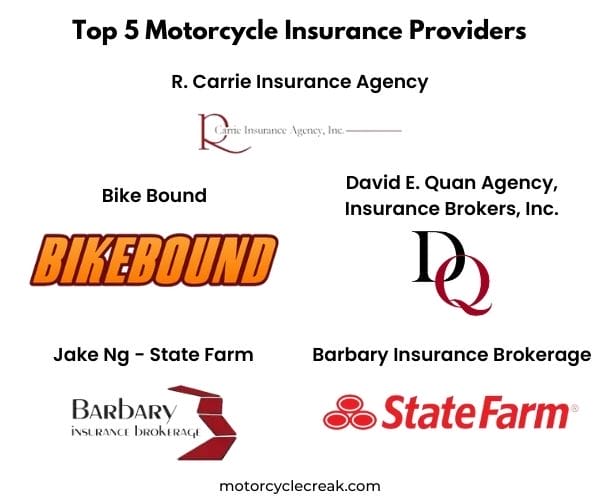

Top Motorcycle Insurance Providers in San Francisco

When choosing motorcycle insurance in San Francisco, finding the right provider to fit your needs is key. Here’s a look at five top-rated companies offering comprehensive options in the area:

1. R. Carrie Insurance Agency

R. Carrie Insurance covers a wide range of motorcycles, including street cycles and ATVs. They offer custom parts coverage, roadside assistance, and discounts for storing your bike in a garage or completing a safety course. Their policies include liability, medical coverage, and uninsured motorist options.

2. BikeBound

BikeBound connects riders with insurers, offering a variety of coverage options like liability, collision, and comprehensive insurance. They focus on helping riders find tailored policies at competitive rates using easy online comparison tools.

3. David E. Quan Agency, Insurance Brokers, Inc.

Serving the entire Bay Area, this agency specializes in motorcycle insurance for all bike types. Their policies include collision, comprehensive, and custom parts coverage, with discounts for bundling policies and completing safety courses.

4. Jake Ng – State Farm

State Farm, through agent Jake Ng, offers motorcycle insurance covering bodily injury, property damage, theft, and emergency expenses. They also provide discounts for safe driving and bundling multiple policies under one plan.

5. Barbary Insurance Brokerage

Barbary Insurance provides comprehensive motorcycle coverage, including theft, collision, and damage caused by uninsured motorists. Additional perks include roadside assistance and custom parts coverage, making them a solid choice for riders looking for full protection.

These providers offer diverse options to meet the needs of San Francisco riders, helping you find the best coverage to fit your bike and budget.

Key Considerations When Choosing a Provider:

- Coverage Options: Ensure they offer liability, collision, comprehensive, and uninsured motorist coverage.

- Discounts: Check for discounts on safe driving, bundling, and safety course completion.

- Customer Service: Look for providers with a solid reputation for responsiveness and smooth claims handling.

- Financial Stability: Opt for insurers with strong financial ratings to guarantee they can pay out claims.

By assessing these factors and comparing quotes, you can find the right motorcycle insurance in San Francisco that fits both your coverage needs and budget.

Conclusion

Riding a motorcycle in San Francisco is an experience like no other—it’s thrilling, scenic, and full of adventure. But in a bustling city with unique risks like high traffic, theft, and unpredictable drivers, having the right insurance is essential. By understanding the local insurance requirements, exploring various coverage options, and taking advantage of discounts, you can protect yourself, your bike, and your finances.

Whether you’re a seasoned rider or new to the city’s streets, investing in comprehensive motorcycle insurance gives you peace of mind. Don’t leave your safety and financial well-being up to chance. Take the time to find a policy that fits your specific needs, so you can focus on enjoying the open road ahead.

Stay safe, ride smart, and enjoy the ride knowing you’re fully covered!

FAQ

Is it illegal to not have motorcycle insurance in California?

Yes, it’s illegal to ride a motorcycle in California without insurance. Riders must carry proof of insurance at all times. Failing to do so can result in fines, license suspension, and even vehicle impoundment, especially if you’re involved in an accident.

What is the minimum insurance requirement in California?

California law requires motorcyclists to have liability insurance with at least $15,000 for bodily injury per person, $30,000 per accident, and $5,000 for property damage. Starting January 1, 2025, these limits will increase to $30,000 per person, $60,000 per accident, and $15,000 for property damage.

What is the minimum motorcycle insurance in California?

The minimum motorcycle insurance in California includes liability coverage of $15,000 per person, $30,000 per accident for bodily injuries, and $5,000 for property damage. These minimums are set to rise in 2025, so riders should consider additional coverage for better protection.